Stage-based fee accounting

We align your income with RIBA work stages and project progress so your accounts are accurate and defensible, and your tax follows what you have genuinely earned.

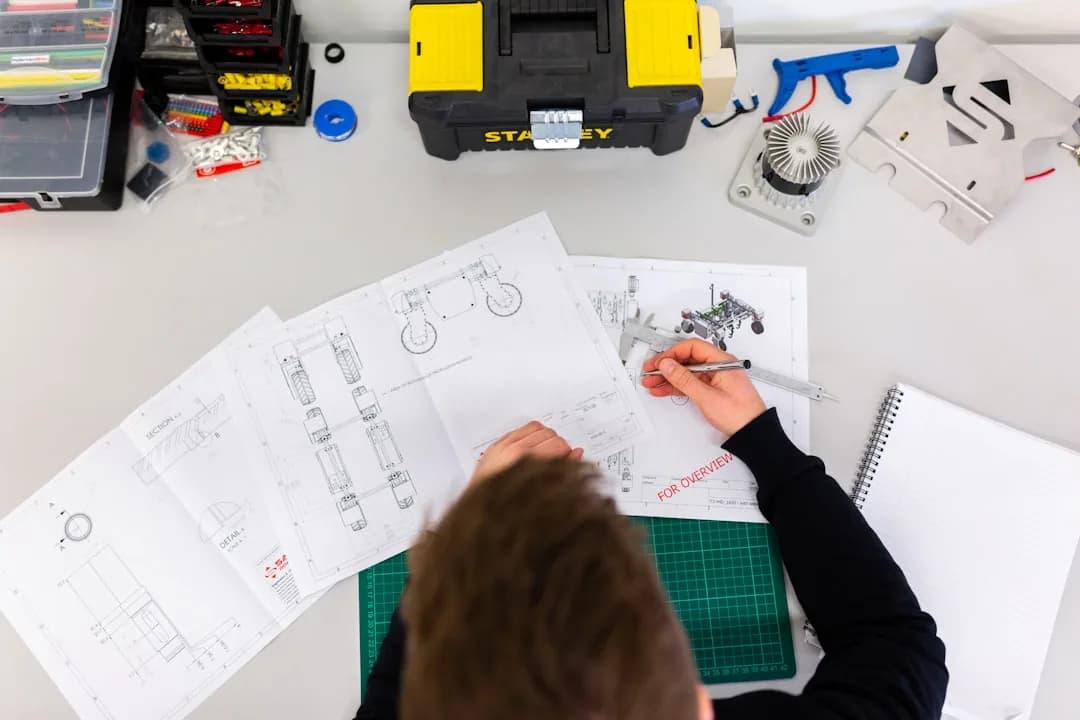

Stage fees, work in progress, PII and your tax return, handled by an architect accountant who works the way your practice actually earns, on one fixed monthly fee.

You design buildings, not spreadsheets. As a specialist accountant for architects, we know your practice does not earn in neat monthly slices. You bill by work stage, you carry half-finished projects across tax years, clients hold back retentions, and you pay run-off professional indemnity cover long after a job is signed off. A high-street accountant treats all that like a corner shop and quietly leaves you out of pocket. Book a call with an architect accountant who follows the project, not the calendar, on one fixed monthly fee.

Most accountants treat an architecture practice like any other small business. They file last year, post your fees as they were invoiced, and miss the things that make your practice different.

They value work in progress wrongly, so a project that straddles two tax years either inflates this year’s profit or hides next year’s. They miss the run-off PII you keep paying after a job ends. They treat ARB and RIBA as personal costs rather than the allowable practice expenses they are. So you overpay, and you never quite know why.

A specialist accountant for architects works the other way round. We know how practices earn, so we know where the money leaks. We do not just record your numbers, we make sure HMRC only takes what it is actually owed.

We align your income with RIBA work stages and project progress so your accounts are accurate and defensible, and your tax follows what you have genuinely earned.

We value and carry half-finished projects across year ends, so a job that spans two tax years does not land you with a lumpy or premature tax bill.

Professional indemnity and run-off cover, ARB registration, RIBA membership, CPD and software subscriptions, all treated for the maximum relief you are entitled to.

We tell you when registration is worth it, get the timing of stage fees right, and keep your returns clean whether you are below or above the threshold.

Your return and accounts filed on time, with the bill flagged months early so January, and your Payments on Account, never catch you out.

Sole practitioner, partnership or limited company, plus how to take money out tax-efficiently through drawings or a salary-and-dividend mix.

This is the one general accountants get wrong. You bill by work stage, often against the RIBA Plan of Work, so a single project can run for months and cross a tax year end with the design half done and the fee only partly invoiced.

If your accountant simply counts the invoices you raised, your profit jumps around and your tax bill rarely matches the work you have actually done. The correct approach is to recognise income as you deliver each stage and to value the work in progress sitting on your desk at the year end, the design effort you have put in but not yet billed.

Get that valuation right and your accounts tell the truth: you pay tax on what you have genuinely earned, not on cash that has not arrived and not on a project you are only halfway through.

We set this up for you and review it every year, so a long, complex job never lands you with a lumpy or premature tax bill.

This flows straight into your Self Assessment or company return, and into bookkeeping that keeps your project income clear all year.

On larger projects, clients often hold back a slice of your fee, a retention, until the work is complete or a defects period has passed. That money is earned but not yet in your bank, and it can sit there for a long time.

If retentions are ignored, your accounts understate what you are owed and your cash flow forecast quietly lies to you. We track every retention and late-stage fee so you know exactly what is outstanding and when it should land.

We then plan your tax and your drawings around real cash, not paper profit, so you are never caught paying a tax bill on a fee a client is still holding.

More than most architects realise. Good accounting for architects starts with claiming every cost your practice genuinely incurs, and your profession comes with a long list a generic accountant would never think to ask about.

On travel you can claim actual running costs or 55p a mile for the first 10,000 business miles, and we work out which one wins. We also keep an architect-specific list so nothing routine gets missed.

Professional indemnity insurance is not optional for an architect, and it is one of your biggest fixed costs. It is fully allowable, and so is the run-off cover you pay after you stop trading or close the practice, sometimes for years.

Run-off premiums are exactly the kind of cost a generalist accountant misses, because they arrive when there is little or no income to set them against. Handled properly, they still reduce the tax on the profit you made in the years you were practising.

We make sure your PII, your run-off cover and your other professional insurances are all claimed in the right period, so you get full relief rather than leaving money with HMRC.

As a sole trader sole practitioner, it is simple. You pay Income Tax and National Insurance on your profits through Self Assessment, usually with Payments on Account, and your accounts stay light.

Bring in a co-director or share profits with another architect and a partnership or LLP may fit better, spreading income and limiting personal liability. Earn more, and a limited company often keeps more in your pocket: you pay Corporation Tax, then take a modest salary and dividends rather than drawing everything as profit.

But a company means more admin, accounts at Companies House, tighter record-keeping and stricter rules on how you take money out. Each structure has real trade-offs.

The right answer depends on your profit, your plans and whether you work alone or with others. We model the numbers and tell you which one puts more money in your pocket.

How you pay yourself depends on your structure. As a sole practitioner or partner, you take drawings, but the tax is on your share of the profit, not on what you happen to withdraw, so we plan your drawings around the bill rather than letting them spring a surprise.

Through a limited company, the usual route is a modest salary plus dividends. The mix matters, because salary and dividends are taxed differently and the most efficient split changes with your profit and your other income.

We work out a sensible, tax-efficient way to take money out, keep you clear of overdrawn director’s loan traps, and make sure you always know what is yours to spend and what to set aside for tax.

Once your taxable turnover passes the £90,000 VAT threshold over a rolling 12 months, registration is compulsory. Many growing practices reach it sooner than they expect, because a couple of large stage fees can tip you over.

Below the threshold, registering can still be worth it if most of your clients are VAT-registered businesses and you carry meaningful costs, since you reclaim the VAT on software, equipment and professional fees.

Stage billing makes the timing of your VAT matter, because the tax point can fall when you invoice a stage rather than when the project completes. We get your VAT registration decision, scheme choice and return timing right, so you neither register too late nor pay more than you need.

Most sole practitioners and small practices pay between £129 and £250 a month. That is a fraction of a single stage fee, and it usually saves you more than it costs through reliefs and structure a generic accountant would miss.

No hourly rates. No surprise bills. One fixed fee, a named, qualified accountant who understands how an architecture practice earns, and a 30-day money-back guarantee.

Startups and small companies that need essential compliance and year-end support without VAT or payroll.

Growing businesses that need complete accounting services, VAT return management, and payroll handling.

Established businesses that want strategic mentoring, business planning, and a part-time finance director driving growth.

I’ve used several accountants in the past, but hands down there is no one better than Harvey at Zmartly. He really understands exactly what advice you’re looking for and explains everything clearly and professionally. Nothing ever feels rushed…

I’ve had an excellent experience working with Zmartly. Harvey and the team are professional, responsive, and genuinely supportive. They explain things clearly, stay on top of deadlines, and always look for practical ways to save tax and improve…

I started working with Zmartly Accountants after having serious issues with my previous accounting firm. They were missing deadlines, incorrectly calculating VAT, constantly late, and extremely difficult and frustrating to communicate with. Switching to Zmartly was a huge…

Have been working Zmartly for nearly 2 years now for my E-Commerce Business and they have been spot on in every aspect. they have given me amazing advice to save tax and they are always on point with…

I've had a terrible experience with multiple accountants. Zmartly have been incredible. If you do ecommerce / Amazon FBA you definitely need to go with someone who understands the complexities with it. Thanks to Harvey and his amazing…

I’ve used several accountants in the past, but hands down there is no one better than Harvey at Zmartly. He really understands exactly what advice you’re looking for and explains everything clearly and professionally. Nothing ever feels rushed…

I’ve had an excellent experience working with Zmartly. Harvey and the team are professional, responsive, and genuinely supportive. They explain things clearly, stay on top of deadlines, and always look for practical ways to save tax and improve…

I started working with Zmartly Accountants after having serious issues with my previous accounting firm. They were missing deadlines, incorrectly calculating VAT, constantly late, and extremely difficult and frustrating to communicate with. Switching to Zmartly was a huge…

Have been working Zmartly for nearly 2 years now for my E-Commerce Business and they have been spot on in every aspect. they have given me amazing advice to save tax and they are always on point with…

I've had a terrible experience with multiple accountants. Zmartly have been incredible. If you do ecommerce / Amazon FBA you definitely need to go with someone who understands the complexities with it. Thanks to Harvey and his amazing…

Stage fees should be recognised as you earn them against contract progress, not simply when you invoice. That means matching income to the work completed on each stage, so your accounts reflect genuine performance rather than the timing of your billing. We set up revenue recognition around your work stages and percentage completion so your profit, and your tax, track the actual project.

Under FRS 102's long-term contract rules, work in progress is valued and carried across the year end so the profit lands in the period it's earned. Without that, a project straddling April can dump a distorted profit (or loss) into one year and skew your tax bill. We value and carry WIP properly so neither year is misstated and your tax stays smooth.

Yes. PII premiums are an allowable trading expense, and run-off cover you pay after a project or after closing the practice is deductible too. So are ARB and RIBA fees, CPD, design software subscriptions, and studio costs. We keep an architecture-specific expense list so recurring professional costs are claimed in full rather than missed.

Generally no, professional services like architecture, surveying, and design consultancy sit outside CIS, so your fees shouldn't have tax deducted at source the way a subcontractor builder's would. But it can get blurred if you take on work that strays into construction operations. We confirm where you fall, so you're neither wrongly taxed at source nor caught out if part of your work does come into scope.

It depends on profit level, whether you're bringing in partners, and how you win work. A limited company is often more tax-efficient once profits grow, while an LLP suits practices with several principals. If you work through agencies or as a sub-consultant, IR35 can apply to those engagements. We model the options and review your contracts rather than defaulting you into one structure.

Plain-English explainers, kept current with the latest HMRC rules.

Zmartly Ltd · 12 Hammersmith Grove, London W6 7AP · 020 8175 5145 · [email protected]

CIMA-regulated. Qualified accountants (ACMA, CGMA, ACCA, FCCA).